Getty Images; Alyssa Powell/BI

By the time she turned 40, Suzie Payne had resigned herself to the fact that she would never be able to buy a home.

While her friends spent their 30s checking off that prized milestone — often with help from their parents — Payne struggled to save money while raising a daughter on her own. Home prices in Portland, Oregon, where she lived, felt out of reach long before the pandemic hit. Then Payne lost her job. When mortgage rates plummeted in the summer of 2020, she was more worried about meeting her basic needs than spending her Saturdays staking out open houses.

In 2021, though, Payne moved to Philadelphia, where the homebuying possibilities seemed to open up. She could still find an old rowhome in the city for a little more than $200,000, well within her price range. She got a new job, took classes for first-time homebuyers, and discovered that she qualified for a larger loan than she'd expected. In the summer of 2024, she enlisted the help of a real estate agent and submitted a winning bid on a house. She was 42.

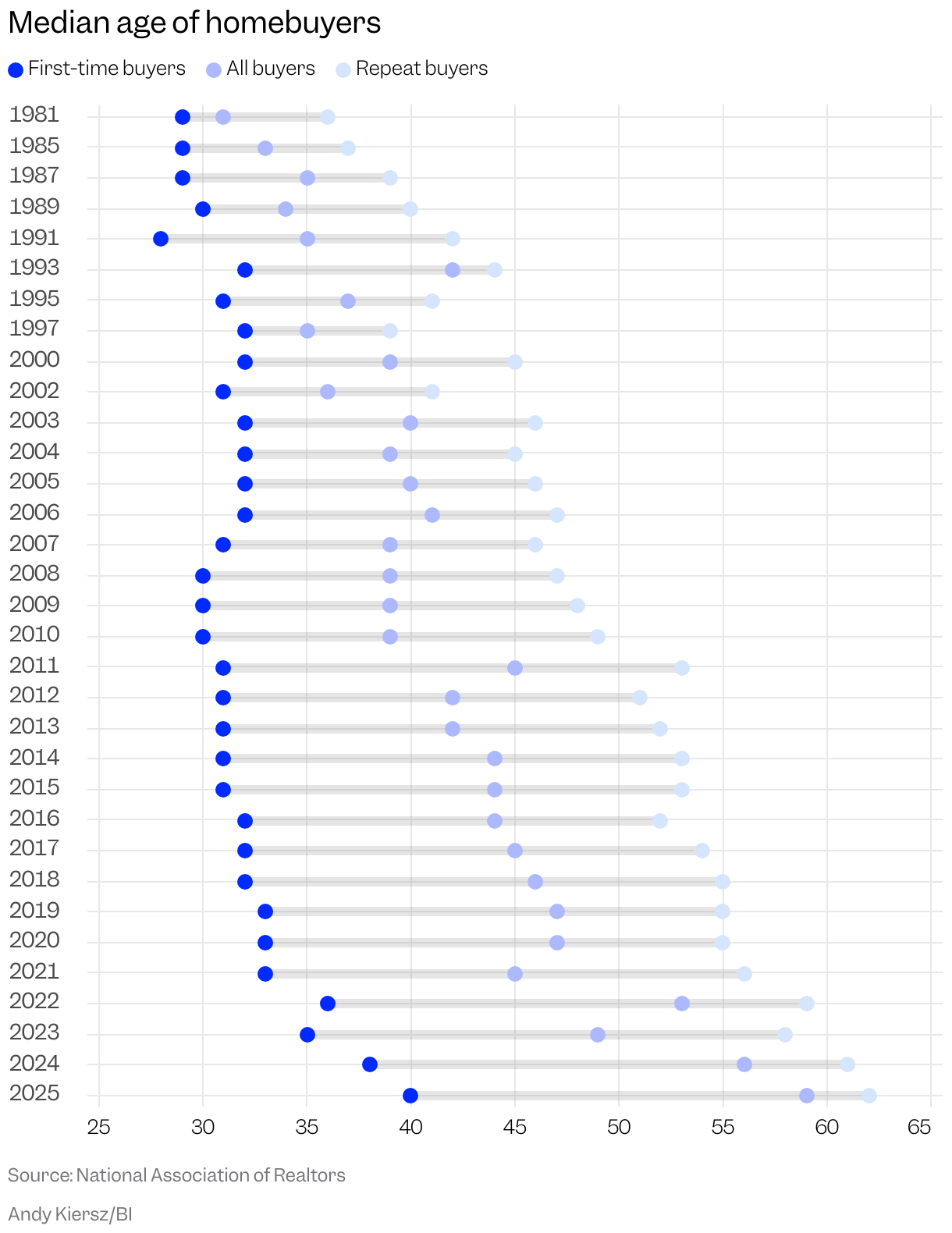

Payne describes her path as "non-conventional," but she represents a sea change in real estate: First-time homebuyers are older than ever. A decade or two ago, Americans typically bought their first homes in their early 30s. By today's standards, however, Payne is right on track. New data from the National Association of Realtors shows that between mid-2024 and mid-2025, the typical age of a first-time buyer reached a record high of 40. The median age for all buyers rose to an all-time high of 59, up from 47 in 2019.

Things have been headed in this direction for a few years now — older, deep-pocketed buyers are better equipped to handle the double whammy of higher borrowing rates and costlier homes. Gen Xers and baby boomers remain active in the real estate market, while the share of purchases by first-time buyers has dwindled. But never before has the divide appeared so stark. This delayed timeline could have lifelong consequences for today's young people: years of missed wealth-building opportunities, fewer moves, even a reevaluation of what constitutes a "starter home." Welcome to the age of the geriatric homebuyer.

The typical first-time homebuyer was just 29 when the NAR began tracking the median age in 1981. The metric edged slightly higher in the four decades that followed, never ticking past 33. Then, between mid-2021 and mid-2022, it spiked to 36. There was a bit of cope around the sudden jump. Maybe it was just elder millennials — long labeled as laggards since graduating into the Great Recession — finally catching up. But even that cohort felt squeezed. Mortgage rates had more than doubled, homes were more expensive, and new construction after the Great Recession had failed to keep pace with the surge of young buyers. I talked to one millennial back then who framed the scenario in bleak terms: "We're royally screwed."

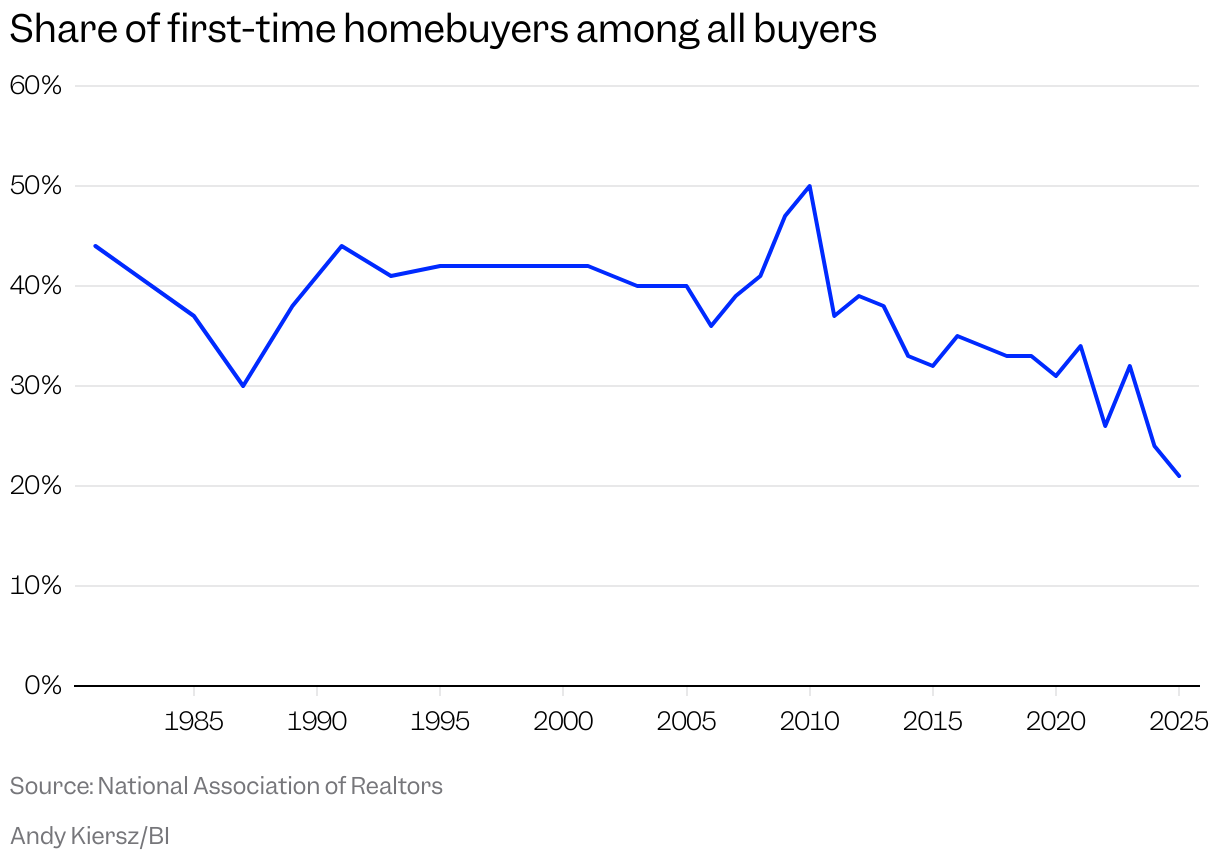

Things have only gotten worse. First-time buyers accounted for a record-low 21% of home purchases last year, NAR data shows — roughly half of the historical average. The entry-level buyer has been effectively "removed from this housing market," Jessica Lautz, the NAR's deputy chief economist, tells me.

"We have a very large young-adult population who are really just seeing the door shut on them for homeownership," Lautz says. "I think it speaks to the gridlock that we've seen in the housing market."

Taking their place is a swarm of "repeat buyers" who, at a median age of 62 (another record high), can put their piles of home equity to work on another purchase. Nearly a third of these repeat buyers paid all cash, NAR data shows, giving them a leg up with sellers who often prefer the ease and speed of deals that don't involve a mortgage. A whopping 26% of all buyers came in with all cash, yet another — you guessed it — record high.

We have a very large young-adult population who are really just seeing the door shut on them for homeownership.Jessica Lautz, deputy chief economist at the National Association of Realtors

Real estate agents tell me they feel the frustration. Peggy Pratt, a broker associate with Century 21 North East in Massachusetts, says it's harder for younger buyers to cobble together a down payment when they're weighed down by student debt and steep rental costs. Pratt specializes in helping people break into the housing market, with about half her business coming from first-time buyers. She says those who are able to gain a foothold often receive help from their parents — there are just fewer of them. On the opposite end, those who can't lean on family "feel that the state of the economy is working against them," Pratt tells me. "For the prices, it's nearly impossible for them."

Suzy Minken, an agent with Compass who works in both New Jersey and northern Virginia, says her clients are no longer buying up "starter homes" with dreams of moving into a bigger place down the line. Most have trouble finding a home they like in their price point, Minken says, so they delay their purchase and keep saving until they can buy a place that feels like less of a stepping stone and more of a permanent landing spot. NAR data backs this up — sellers last year had lived in their homes for a median of 11 years, an all-time high.

"The idea of move-up buyers, I think we're sort of done with that," Minken says. "It doesn't really happen. People that I've sold homes to over the years, no one's moving up to get a bigger home."

All of this contributes to the gridlock Lautz mentioned. First-time homebuyers benefit from churn in the housing market: When people move out of their theoretical starter homes into bigger places, they free up the entry-level homes for those just starting out. But that sort of healthy movement has ground to a halt. After the steep rise in mortgage rates a few years ago, homeowners are holding tight to the rock-bottom terms they secured earlier in the pandemic. Until rates sink further or they're forced to make a move, those owners are not going anywhere. And if people are waiting longer to buy their first house, they may have already checked off the other significant milestones, such as having children, that could prompt another move anyway.

There's some upside to purchasing later in life: If you buy your first home at 40 instead of 30, you're likely closing in on your peak earning years. You may have a better sense of your family's needs and where you want to live. While it's nice to have a bit more certainty before taking the homeownership plunge, the downsides can be brutal. By delaying, you've also missed out on years of potential wealth-building. Given that homes tend to gain about 5% equity on an annual basis, the typical homeowner is foregoing about $150,000 if they buy a decade later than the historical norm, Lautz tells me. That wealth could be used to purchase the next home, fund their child's college education, or make needed upgrades to their existing place.

"We're looking at a generational wealth restriction," Lautz says.

Suzie Payne's homebuying journey didn't end with that accepted offer. Her daughter had a medical emergency around that same time, she tells me, forcing her to back out of the purchase. In March, she took another stab at buying and had a second offer accepted. But Trump's looming tariffs made her uneasy about the economy, and an inspection on the house revealed a heap of necessary repairs. When negotiations broke down, Payne backed out of that deal as well.

"I was like, I can't do this right now," Payne tells me. "It's so emotional and overwhelming and scary when you are the only financial conduit for this huge purchase."

Payne's series of stops and starts effectively captures the current homebuying predicament. Buyers are older, sure, but they're also pulling out of deals more frequently than ever, either because they're spooked by the economy or holding out hope for a better deal down the line. Consumers of all stripes are wary of making big life changes that could leave them in a tough financial situation if things go awry. For Payne, a home purchase was never about the investment, anyway — it was about finally achieving stability in a place where a landlord could never raise her rent overnight. Until she feels like a home purchase would give her peace of mind rather than more worries, she's prepared to play the waiting game.

"It has to be the right conditions," Payne tells me. "And right now does not feel like the right conditions."

James Rodriguez is a correspondent on Business Insider's Discourse team.