Getty Images; Tyler Le/BI

Jean Frohling always wanted to help her three children buy places of their own. She and her husband, now in their mid-60s, saved for years in hopes of one day pulling their kids onto the property ladder. Eventually, hard work and foresight paid off: They gifted each of their first two children thousands of dollars to pad the down payments on their first homes.

Then, about a year ago, their youngest daughter found a house she liked just outside Peoria, Illinois. The Frohlings figured their then 33-year-old daughter could probably afford the house on her own, but they decided to leave even less to chance this time. They wanted to make sure their daughter avoided a mortgage hiccup or, worse, losing out to a stronger offer. Frohling and her husband opted to buy the home outright, paying $186,000 in cash.

"We just felt there was some negotiation power in the cash offer, and that it would ease the transition," Frohling tells me.

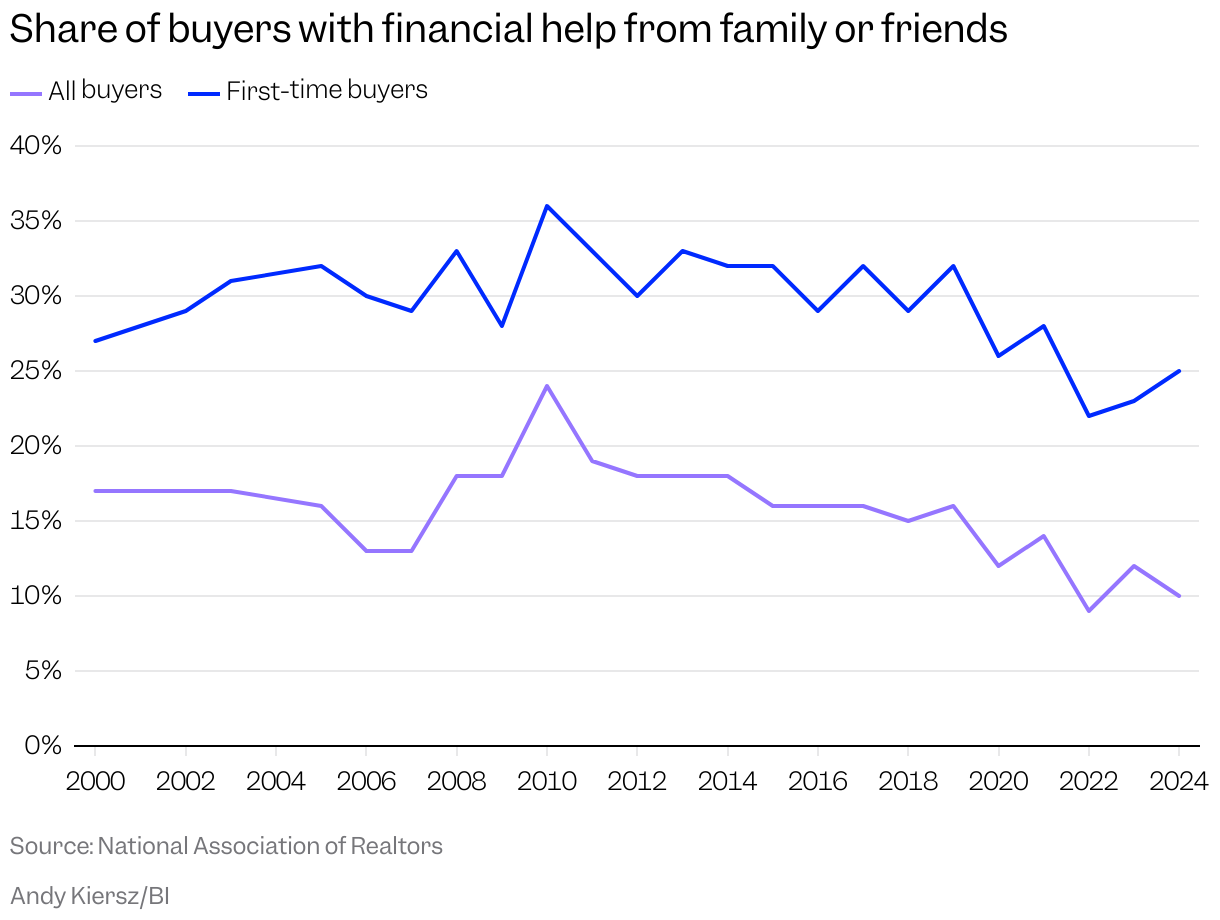

Nepotism is a hot topic these days: So-called "nepo babies" seem to be everywhere, riding the coattails of their rich and famous parents to land starring roles in movies, record Billboard hits, and wield power in Washington. The housing market isn't Hollywood, but as long as families have had a few dollars to pass down from one generation to the next, youngsters have relied on help from parents to get their foot in the door. Over the past three decades, about 30% of first-time homebuyers each year used a gift or loan from family and friends, data from the National Association of Realtors shows. For buyers of all types, family swooped in to help about 16% of the time.

Conditions would appear ripe for nepo buyers' numbers to spike — with prices high and borrowing rates still steep, lots of home shoppers could use a hand. Many baby boomers are sitting on piles of home equity or bulging investment portfolios that they could theoretically tap to aid their millennial and Gen Z offspring. Yet the nepo homebuyer is actually in decline. The past few years of NAR data have shown a significant dip from the historical average: In 2024, only a quarter of first-time buyers got help from friends and family. For all buyers, this share has slipped to just 10%.

This downturn defies conventional thinking. The market has been so brutal for young buyers that it can be hard to imagine someone making it onto the housing ladder without a boost. Are selfish boomers turning their backs on their kids? Has the bank of mom and dad run dry? The latest numbers suggest something else is going on: The buyers breaking into the market don't actually need the assist.

"This is a different type of first-time homebuyer than we've seen historically," Jessica Lautz, the deputy chief economist at NAR, tells me.

For those forced to rely on their humble savings accounts, all of this may sound encouraging: Fewer nepo buyers might mean better odds for everyone else. But the trend points to troubling changes in the housing market's makeup. Ironically, the thinning ranks of nepo buyers may be yet another sign that something's amiss.

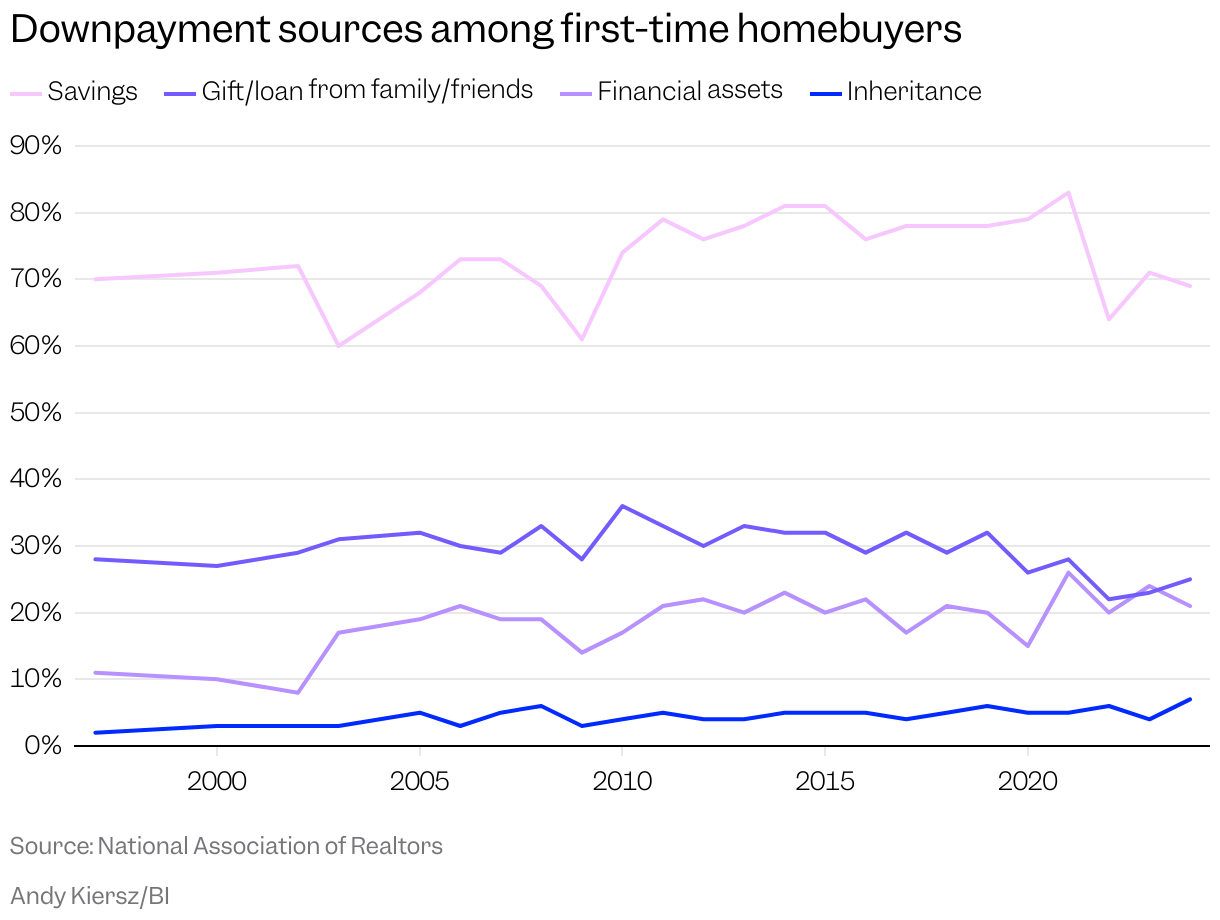

Like it or not, the bank of mom and dad plays a crucial role in propelling Americans into homeownership. Elder family members with the means to do so may chip in money for a down payment, extend a friendly loan with below-market terms, or simply buy a house and put their kid on the title, like the Frohlings did. In 2019, according to NAR, a whopping 32% of first-time buyers — and 16% of all buyers — leveraged some help from family and friends for their home purchase. Figures like these were not uncommon. In fact, NAR recorded the highest percentage of nepo buyers in 2010, when 36% of first-time buyers and 24% of all purchasers fell into this camp.

"I do think that family has always played a role," Lautz tells me.

This kind of assistance isn't limited to the ultrawealthy. Chase Rogers, a mortgage loan officer in Birmingham, Alabama, where the median sale price is about $190,000 — well below the national median of more than $440,000 — says he's recently seen middle-class buyers use family help to slightly level up their purchase. These kinds of buyers, he says, "can qualify for something without help from their families, but then to get something more to their taste, maybe a little bit higher price range, they are getting help."

This is a different type of first-time homebuyer than we've seen historically.Jessica Lautz, deputy chief economist at the National Association of Realtors

Geoff Black, a mortgage loan officer in Sacramento, California, watched family money pour into the market during the COVID-era frenzy. Back then, he says, the prevailing attitude among parents was, "You need to get in right now." The housing market was a runaway train, and you either hopped on or got left in the dust.

"I literally remember talking to a parent as she fired off $350,000 as a gift," Black tells me. "She mumbled, 'Get me some grandbabies.'"

Millennials and first-time buyers back then had no illusions about the chaos sweeping through the market. One guy I talked to in late 2022, a young millennial who, by a stroke of luck, managed to lock down a place after months of searching, pronounced his cohort "royally screwed." The affordability barriers have only continued to rise. The median home price is up roughly 37% since July 2020. Mortgage rates have drifted down but are still hovering at about 6.4%, more than double the record-low rates buyers got at the height of the pandemic. A recent Bankrate study found that the household income required to afford a typical home has surged to nearly $117,000, up from about $78,000 in early 2020. And it's not as if young buyers don't think to use their families as a lifeline. A Redfin survey last year found that more than a third of Gen Zers and millennials who planned to buy a home soon said they expected to use a cash gift from family to fund their purchase.

As affordability has only gotten worse over the past few years, purchases with gifts have — bafflingly — faded. Black says gift-giving seemed to peak around 2021 or early 2022, right when NAR's data began showing a decline in nepo buyers' market share. After hovering around 27% in 2020 and 2021, just 22% of first-time buyers got help from family or friends in 2022, the lowest on record. The following year showed only a slight uptick, to 23%. Last year, just a quarter of first-timers got that kind of assistance.

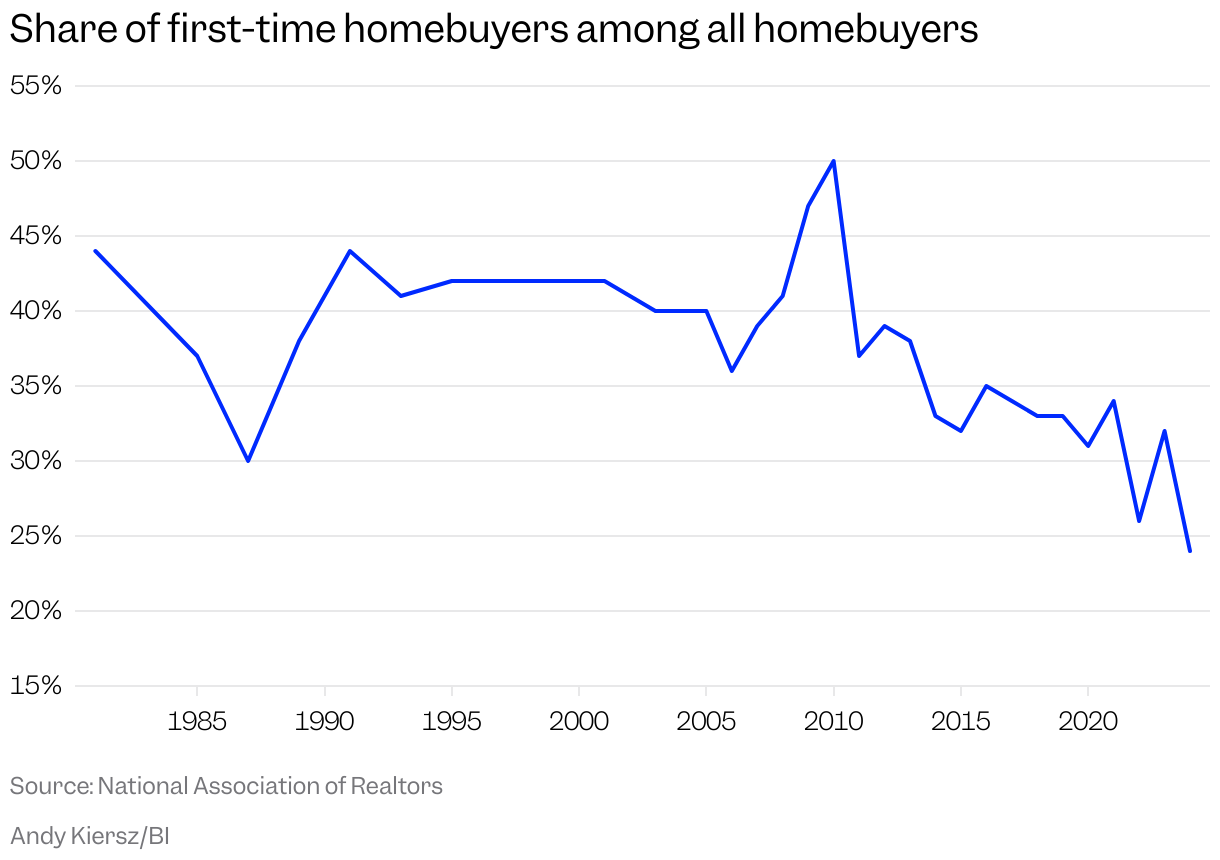

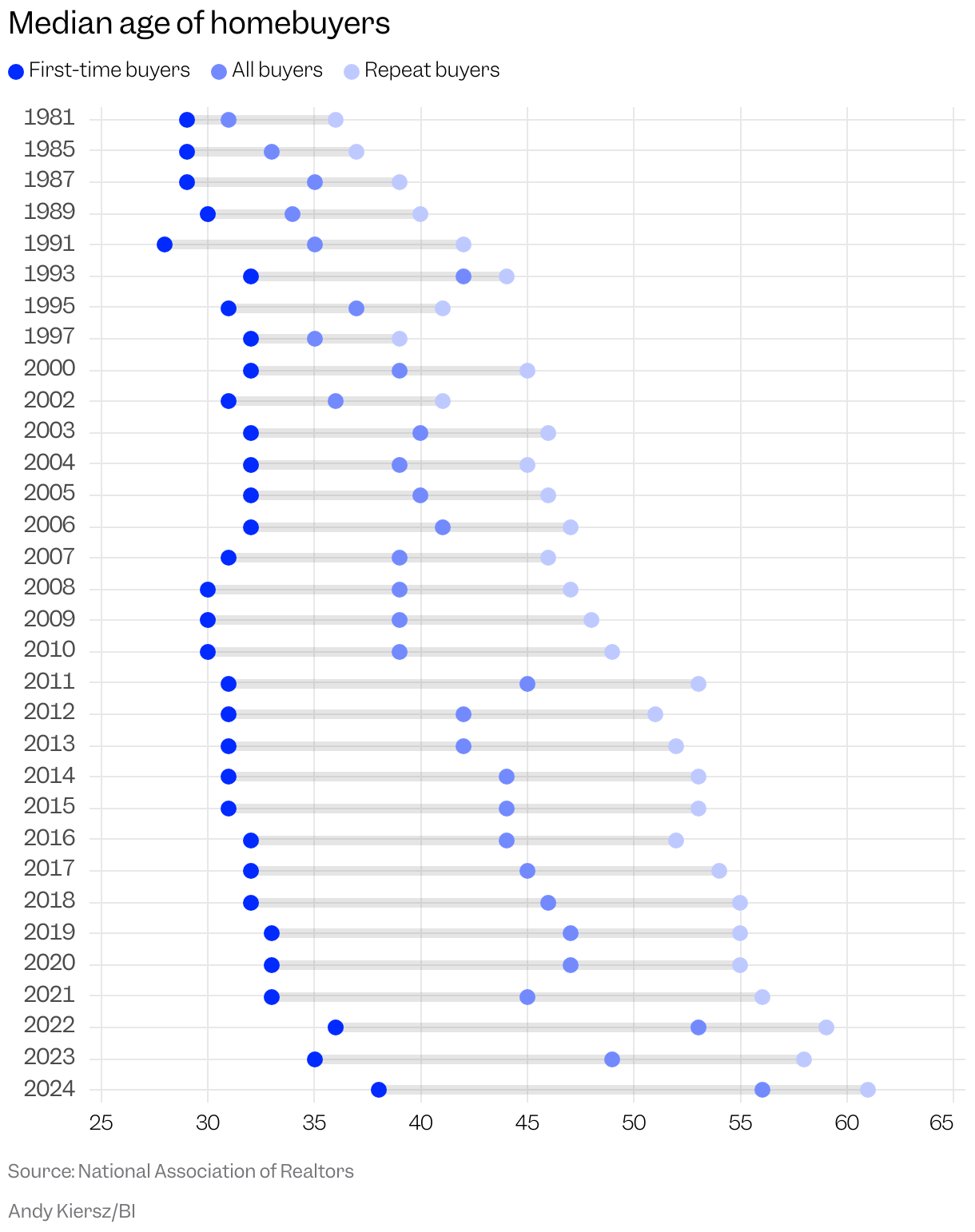

The decline of nepo buyers also coincides with another big shift in the makeup of new homeowners: First-time buyers are older and winning out with less frequency than ever before. NAR data shows that between June 2021 and June 2022, the typical first-time buyer was 36, the highest median age since NAR started tracking the figure in 1981. New homeowners accounted for a bit more than a quarter of all home purchases, a record low. Things have only gotten worse. The typical age of a first-time homebuyer last year hit another all-time high of 38, NAR data shows. First-time buyers' market share also shrank to a new low of just 24%, down from 32% the year prior. Perhaps unsurprisingly, buyers who made it through the door were better funded than in years past — the median household income of first-timers was $97,000, a jump of $26,000 in two years.

These shifts help explain the nepo-buyer pullback. Family help is less common because the market is dominated by older, more independent buyers who can push forward despite the affordability challenges. Each year that prospective homeowners kick the can down the road, they grow less likely to ask for a family handout. NAR found last year that younger millennials, which it defined as ages 26 to 34, got gifts from family at about twice the rate of the elder cohort, ages 35 to 44.

"It becomes more uncomfortable for someone who's 38 years old, which is the median age of today's first-time homebuyer, to ask for mom and dad's help to purchase a home," Lautz says, "as opposed to someone who is in their late 20s or younger 30s."

This shift could have ripple effects throughout this cohort's entire lives. Older first-time homebuyers miss out on years of home-equity building, contributing to what Lautz often refers to as a "housing economy of 'haves' and 'have-nots.'" Instead of people embarking on their homeownership journey with a little help from their parents, they're staying put entirely.

"To me, it's a sign of buyer weakness when that gifting is pulling back," Black tells me.

As I noted in a recent story about homebuyers' cold feet, the fear of missing out that defined the early-COVID market has given way to a different flavor of FOMO. People are wary of taking the homebuying plunge given the state of the world: The job market is wobbling as executives pull back on hiring and warn of permanently smaller headcounts. Student-loan delinquencies are spiking. In light of the staggering costs of homeownership, an analysis by the housing research firm Zelman concluded that the rent-versus-buy math favors renting to a degree that hasn't been seen since the early 1980s. Prospective buyers may also be counting on borrowing rates to drop or sellers to slash prices even further.

With those on shakier ground hanging back, the buyers forging ahead are older and wealthier than at any point in more than four decades. They're relying more on their own investment accounts and less on the bank of mom and dad. The nepo buyer has taken a back seat.

Of course, parents can pass along privilege in all kinds of ways that aren't clear at the closing table. Paying for college tuition, say, can ensure their child graduates debt-free and ready to stack savings. Children whose parents are homeowners are more likely to end up buying a home themselves. A growing number of first-time buyers are moving straight out of their parents' places, saving on rent before heading out on their own. Even homebuyers who don't get a financial handout may benefit from the advice and know-how of parents who have already weathered the process.

To me, it's a sign of buyer weakness when that gifting is pulling back.Geoff Black, mortgage loan officer in Sacramento, California

But cold, hard cash remains the simplest way to get a foothold in the market. That kind of help doesn't always equate to a free ride, though. Roughly a year after Frohling and her husband purchased the Illinois home, their daughter refinanced to pull equity out of the house to pay her parents back. The maneuver leaves a new loan attached to the place, which their daughter will now begin the long process of paying off — and building a nest egg of her own.

While nepo buyers' numbers are down, they're far from extinct. Bill Mitchell, the loan officer who helped the Frohlings execute the refinance, says it's hard to overstate the power of a cash offer in a competitive market like Illinois, where a relative lack of homebuilding means the number of homes available for sale is still tight. Mitchell estimates that about 20% of his clients use family money to beef up their offers.

"When I see that situation, and I see that I've got these clients that have made an offer on one, two, three homes and got beat out by cash offers, that's typically when I'll say, 'Hey, let's think of potential alternative strategies here,'" Mitchell tells me. "'Do you have family that would be willing to help out in a situation like this?'"

Frohling says she initially worried she had robbed her daughter of the joy that comes with buying something all on your own after years of saving. But for Frohling's daughter, homeownership didn't come without sacrifice: She and her husband, for example, skipped throwing a big wedding and saved that money instead. And in the end, Frohling tells me, the ease and convenience were worth it.

"I know that we are blessed to be able to do that," Frohling says.

James Rodriguez is a senior reporter on Business Insider's Discourse team.