TMTPOST – China’s photovoltaic (PV) sector is at a critical juncture as domestic policies aimed at curbing overcapacity collide with the rapid expansion of India’s solar manufacturing industry. While Chinese authorities push for “anti-involution” measures to consolidate capacity and reduce internal competition, overseas PV markets, particularly in India, are growing quickly, raising questions about long-term strategic positioning.

AI-generated image

At a July 3 symposium, MIIT Minister Li Lecheng emphasized that China fully supports PV companies expanding overseas. However, he stressed that key technological links must remain under domestic control to ensure China maintains a leadership advantage in advanced generations of PV technology.

Industry leaders are now weighing the potential downside of aggressive anti-involution policies. Cutting domestic production capacity—even for relatively new facilities—may inadvertently cede international market opportunities to competitors abroad. Countries ramping up solar capacity are often strategic rivals, prompting concerns about transferring advanced production capabilities without sufficient safeguards.

India’s largest private conglomerate, Reliance Industries, has announced plans to invest more than 600 billion Indian rupees (approximately $8.1 billion) over the next three years to establish large-scale solar factories, energy storage, electrolyzers, and fuel cells. An additional $2 billion will be allocated for developing the full value chain and future technologies.

Chinese PV equipment companies are central to these plans. In 2022, Maiwei Co., Ltd., through its Singapore subsidiary, signed a contract with Reliance to supply eight HJT cell production lines totaling 4.8GW, valued at more than half of Maiwei’s 2021 revenue. Despite the significance of this contract, the company has provided minimal disclosure on revenue recognition, citing publicly available information. Maiwei is also pursuing refinancing in China to expand perovskite equipment production.

Reliance’s first gigawatt-scale HJT module production line went online in April 2025, supported by Chinese suppliers. SC Solar, a subsidiary of Kingsemi, supplied automated module production lines with a capacity of 5.2GW, the largest domestically built heterojunction module line in India, highlighting the reliance of India’s solar manufacturing ambitions on Chinese technology.

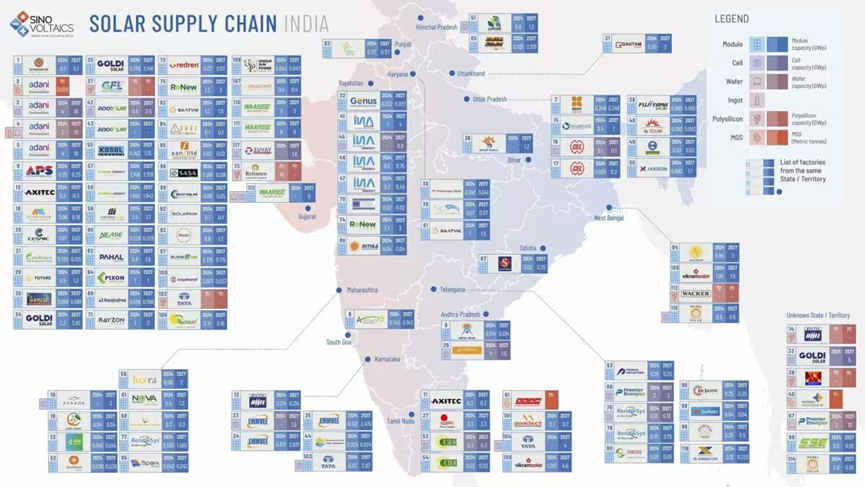

(India Solar Supply Chain Map. Source: Sinovoltaics)

India Hits 100GW of Solar Capacity

India’s government reported that non-fossil fuel power generation now constitutes nearly 50% of the nation’s total, with solar PV reaching 116GW, achieving the country’s 2030 Paris Agreement target five years ahead of schedule. Domestic manufacturing has also surged, driven by the Production Linked Incentive (PLI) scheme, which has added 18.5GW of module capacity, 9.7GW of cell capacity, and 2.2GW of silicon ingot and wafer capacity.

ALMM certification policies, which restrict government-funded projects to approved domestic suppliers, alongside 40% tariffs on imported modules and 25% on imported cells, have created a protective framework enabling India’s solar industry to expand rapidly. India’s approved PV module manufacturers now total 100GW in capacity, with cell manufacturers at 13GW, of which only 3.3GW is TOPCon technology. Most of the current 100GW of capacity is concentrated in module assembly, leaving cell and wafer production heavily dependent on imports, primarily from China.

China’s General Administration of Customs reports that in the first half of 2025, exports of solar cells to India reached 5.925 billion RMB, a 46.6% year-on-year increase, demonstrating India’s continued reliance on Chinese products. However, equipment exports remain less transparent, raising strategic concerns about technology transfer and generational gaps.

Indian regulations increasingly aim to move from module assembly to full-cell manufacturing. The Ministry of New and Renewable Energy mandates that future projects use cells produced from completely undiffused silicon wafers—banning the previous practice of importing semi-finished “Blue Film Wafers.” By June 2026, government-supported projects must use ALMM List-I modules and List-II cells, enforcing end-to-end supply chain control and boosting local production capacity.

This shift underscores India’s strategy to strengthen its domestic cell manufacturing and reduce dependence on imports. In the near term, India aims to expand domestic cell capacity to over 30GW by 2027, implying a nearly 20GW increase in the next two years—a market opportunity heavily weighted toward Chinese equipment suppliers.

China maintains a dominant 90% market share in PV equipment, giving domestic manufacturers significant leverage. Historically, exports were facilitated by Chinese companies establishing factories in Southeast Asia. However, with stricter anti-dumping measures and rising demands for localized production, equipment manufacturers face a complex crossroads.

The United States, historically the most profitable market, imposes strict restrictions on Chinese PV equipment, while Europe remains a small and fragmented market. In contrast, India offers scale, policy support, and a labor force to support localized manufacturing, making it an attractive—but strategically sensitive—market.

The central question for China’s PV industry is how to balance domestic consolidation with overseas expansion. Unchecked export of advanced equipment could empower Indian manufacturers, reducing China’s influence in overseas module markets and intensifying competition. While labor and operational yields in India may lag behind Chinese standards, rising Indian competitiveness could erode overseas profit margins for Chinese companies.

Unlike other critical technologies, such as advanced lithography machines or lithium battery materials, China currently imposes limited restrictions on exporting high-end photovoltaic equipment. The 2023 “Catalogue of Technologies Prohibited or Restricted from Export” lists large-size silicon wafer technologies but does not explicitly include PV cell manufacturing equipment. As a result, equipment manufacturers have few regulatory constraints when pursuing overseas sales, although broader strategic responsibilities may lie with regulators.

Experts suggest that as India expands its domestic solar manufacturing capabilities, Chinese authorities may need to implement targeted restrictions or safeguards to maintain technological leadership and prevent the erosion of competitive advantages.

China’s PV industry faces a strategic balancing act. Domestic “anti-involution” policies aim to consolidate capacity and reduce destructive competition, but rapid expansion in India highlights the risks of ceding influence in global markets. As India accelerates toward local cell production, Chinese equipment manufacturers will continue to play a key role—but unchecked technology transfer may create long-term competitive challenges.

India’s growing solar market, young labor force, and aggressive industrial policies position it as a formidable competitor. With domestic PV capacity still navigating consolidation challenges, China must carefully calibrate policy, regulation, and export strategy to maintain its global leadership. The coming months will be critical, as regulators and industry leaders weigh anti-overcapacity measures against the strategic imperative of safeguarding China’s technological edge.

更多精彩内容,关注钛媒体微信号(ID:taimeiti),或者下载钛媒体App